DUTIES OF DIRECTORS UNDER THE COMPANYS ACT

Directors do not generally owe their duties to anyone other than the Company, nor fiduciary duties to individual members.

The general duties are owed by a director of a company to the company are:

- To act within powers ie

- Act in accordance with the constitution of the company.

- Do not act in excess of the powers conferred too them by the company’s articles.

- To promote the success of the company. A director should act in good faith, in a manner that would promote the success of the company for the benefit of its members as a whole. The shall have regard to:

- The long-term consequences of any decision of the directors;

- The interests of the employees of the company

- The need to foster the company’s business relationships with suppliers, customers and others;

- The impact of the operations of the company on the community and the environment.

- The desirability of the company to maintain a reputation for high standards of business conduct.

- The need to act fairly as between the directors and the members of the company

- To exercise independent judgment. This duty is not infringed by the director acting in accordance with an agreement duly entered into by the company that restricts the future exercise of discretion by its directors or where director acts in a way authorised by the constitution of the company. – This goes to show that they should ensure they know which types of contracts they are entering into (Consult KIOI & CO for your contracts)

- To exercise reasonable care, skill and diligence – Ensure that you conduct due diligence, compliance, KYC measures etc.

- To avoid conflicts of interest. A director of a company shall avoid a situation in which the director has, or can have, a direct or indirect interest that conflicts, or may conflict, with the interests of the company.

- Not to accept benefits from third parties if the benefit is attributable to the fact that the person is a director of the company or to any act or omission to the person as a director – NOTE: Where that gift does not amount to conflict of interest, it is not an infringement. Conflict of interest includes conflict of duties.

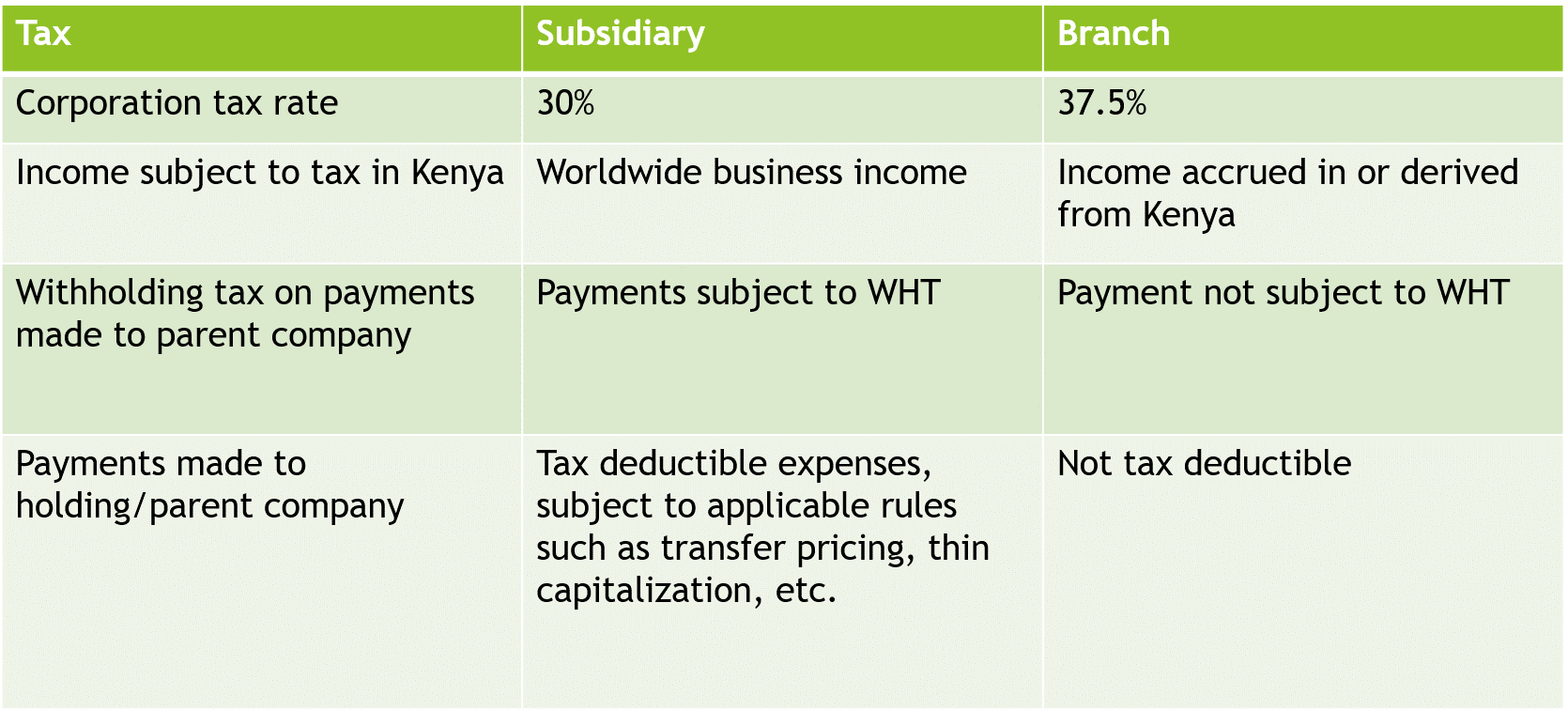

Taxes Founders/Directors and CEOs should know about

- Corporation tax

- Instalment tax

- Instalment tax applies to business entities as well as individual persons who pay more than KShs. 40,000 in tax per year and whose income is not taxed under PAYE.

- Installment taxes are not however payable by persons who are subject to Turnover Tax (TOT)

- It is a form of advance tax paid to KRA. Hence, it is claimed as an advance payment made in the given year of income.

- Turnover tax

- Turnover tax (TOT) (section 12C) is payable by a resident person whose turnover from business is more than Kshs. 1 million and does not exceed or is not expected to exceed KShs. 50 million shillings during any year of income.

- Withholding tax

- Withholding tax is applicable to income received from Kenya by way of management and professional fees, rents, interest, dividends, royalties and such other passive or specified income.

- The withholding tax rates differ, depending on whether the payments are made to Kenyan residents or to non-residents and on tax treaty rates where applicable.

- Withholding tax is due upon payment and remitted to the Commissioner by the 20th day of the month following the month of deduction.

- The payer is also required to issue the payee with a withholding tax certificate.

- basis, on or before the 20th day of the following month that the digital service was offered.

Pay as You Earn (PAYE)

- PAYE is the liability imposed on an employer to deduct and remit tax on the employment income of the employees. (These include directors).

- PAYE is due on the 9th day of the following month.

An employer files monthly returns (previously, an employer could file monthly or quarterly returns).

NSSF Rates – Employer Obligations

- Every employer who engages one or more employees is required to promptly register with NSSF as a contributing employer;

- Ensure prompt registration of all employees as members of NSSF;

- Promptly deduct and remit contributions in full by the 15th day of the following month. Late payments of mandatory contributions shall attract a penalty at the rate of 5% of the total contributions for each month or part of the month that is remitted late;

- Promptly submit accurate monthly returns in the prescribed format by the 15th day of the following month;

- Maintain proper and up to date records of employees’ earnings and particulars.

- An employer who fails to comply with the above commits an offence.

NHIF Rates

The rates are based on gross monthly income. The lowest contribution shall be Ksh 150 for incomes up to Ksh 5,999; the highest contributions are at Ksh 1,700 for incomes over 100,000.